Remember me

CUSIP 912828N71 continued the trend of strong performance.

By David Enna, Tipswatch.com

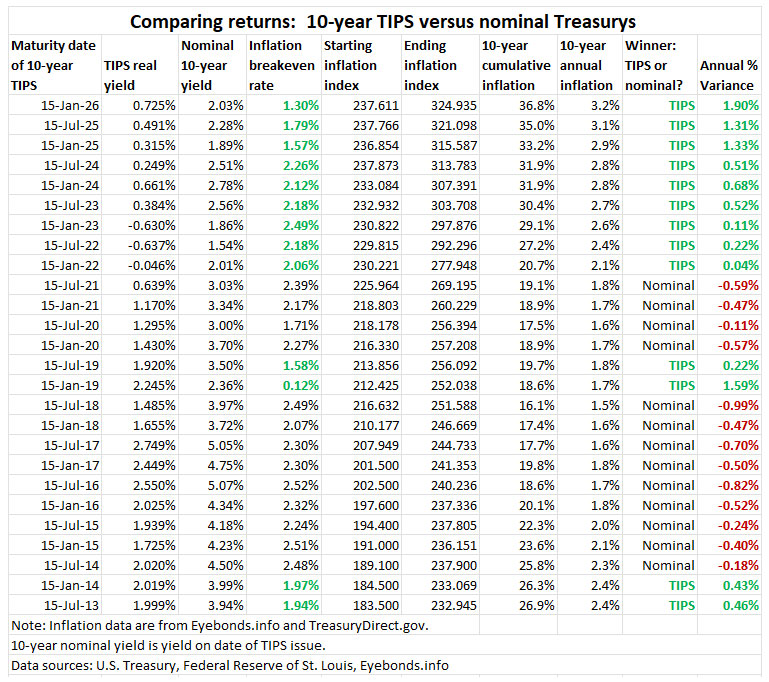

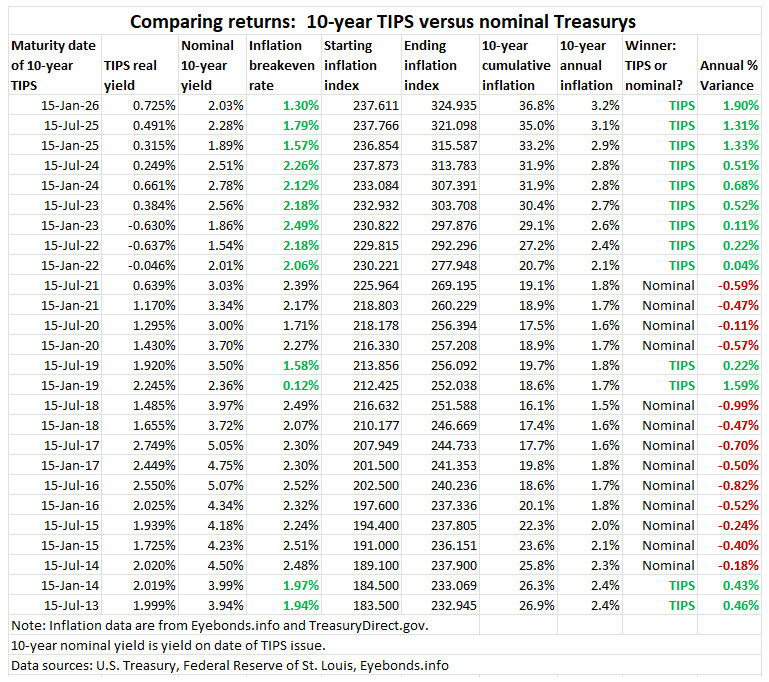

Back on Jan. 21, 2016, we had a “sort-of” exciting moment in the market for Treasury Inflation-Protected Securities. The Treasury auctioned a new 10-year TIPS — CUSIP 912828N71 — which generated a real yield to maturity of 0.725%, the highest yield for any 9- to 10-year TIPS auction for nearly five years.

That real yield seems mundane today, but it was a big improvement over a stretch of very low and often negative real yields dating back to September 2011.

Inflation breakeven rate. Another interesting aspect of this TIPS is that on the auction date the 10-year nominal Treasury note was yielding just 2.03%, creating an ultra-low inflation breakeven rate of 1.30%.

Let me ask: Do you think inflation averaged more than 1.3% over the last 10 years? The answer, of course, is yes. Inflation averaged 3.2% over the next 10 years, making this TIPS an outstanding investment versus the 10-year nominal bond of the time.

The final investment results for this TIPS were set by the “iffy” November inflation report released Dec. 18, which may have slightly under-reported true inflation because of problems with government data collection. We will never know for sure. Here is how CUSIP 912828N71 performed at the end:

Data from Eyebonds.info show this TIPS generated a 10-year nominal annual return of 3.902%, easily exceeding the comparable nominal Treasury at 2.03%. For its time, CUSIP 912828N71 was a very good investment.

TIPS versus an I BondAn I Bond issued in January 2016 had a fixed rate of 0.10%, well below the real yield of this TIPS at 0.725%. According to Eyebonds.info, from January 2016 to the end of June 2026, the I Bond will have generated a nominal return of 3.16%. That is better than the Treasury note at 2.03%, but lags the return of the TIPS at 3.902%.

TIPS versus other alternativesThe total bond market, defined by Vanguard’s Total Bond ETF (BND), has had an average total annual return of 1.94% over the last 10 years, trailing both the January 2016 I Bond and CUSIP 912828N71.

The TIP ETF, which holds all maturities of TIPS, has had an average total return of 2.86% over the 10 years. VTIP, the short-term TIPS ETF, had an average return of 3.15%.

So, when compared to safe alternative investments, CUSIP 912828N71 had the best performance.

One more thing: CUSIP 912810FS2Another TIPS is maturing Jan. 15: CUSIP 912810FS2, a 20-year TIPS that was originally auctioned on Jan 24, 2006. I don’t track the old 20-year maturities because the Treasury stopped issuing them in November 2009. This TIPS was attractive, with a real yield to maturity of 2.039% at the originating auction.

At the time, a 20-year Treasury bond was yielding 4.63%, giving this TIPS an inflation breakeven rate of 2.59%. Over the last 20 years, annual inflation has averaged 2.51%, and this TIPS will end up providing a nominal return of 4.512%, slightly below the nominal Treasury.

Verdict: CUSIP 912810FS2 was a slight loser versus the nominal Treasury. This happened because inflation ran at lower-than-predicted levels much of the time through 2020.

ThoughtsThere is an obvious lesson here: TIPS do well when inflation is higher than expected, and that is exactly why we invest in TIPS — to protect against that possibility. When compared to similar investments, buying this 10-year TIPS in January 2016 and holding to maturity was a sound move.

I purchased this TIPS in a taxable account at TreasuryDirect with a small investment at the January 2016 auction. I get my payday on January 15.

TIPS have been on a winning streak for several years, caused by the surge to 40-year high inflation that peaked in June 2022 at 9.1%. Even today, annual inflation (2.7%) is running higher than the auctioned breakeven rate of January 2016. And so TIPS have been the winners versus nominal Treasurys in recent years.

See historical data on my TIPS vs. Nominals page.

Notes and qualifications

See historical data on my TIPS vs. Nominals page.

Notes and qualifications

My chart is an estimate of performance comparing inflation breakeven rates versus actual inflation.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I plan to keep it that way. Some readers have suggested having a way to contribute. I would welcome donations. Any amount, or skip it, your choice. This is completely optional.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Comments (0)